The tech-luxury revolution is rewriting the rules of automotive prestige. German brands must act now — or risk becoming relics of a bygone era.

By Steffen Edlinger | March 2026 | Edlinger Strategy & Consulting

The End of an Unwritten Law

For decades, German automakers didn’t just participate in the premium market — they defined it. Mercedes, BMW, Audi: these weren’t merely brands, they were statements. Statements for engineering supremacy, uncompromising quality, and a kind of industrial dominance that competitors could admire but never replicate. A Porsche Cayenne and a VW Touareg shared the same platform and nearly identical powertrains — yet the Cayenne commanded nearly double the price. An Audi A3 was, technically, a VW Golf in a different suit — and still delivered significantly higher margins. The price premium of 20–30% over volume competitors was not a marketing trick.

It was an unwritten law of the automotive world – one that paid off. Together, Volkswagen, BMW, and Daimler at their peak contributed roughly 40% of all DAX profits. No other national automotive cluster came close. However, this law has been broken.

How the Powertrain Shift Reshuffled the Game

The battery electric revolution didn’t just change what sits under the hood. It fundamentally altered what consumers consider „premium.“ Tesla was the catalyst — not because it built a better car in the traditional sense, their built quality and gap tolerances were ridiculed by German OEMs to be far inferior to the „German standard“. But because it created an entirely new category. By defining the battery electric vehicle as a product category and redefining user experience through software, Tesla positioned itself as a status symbol for affluent tech enthusiasts before expanding to the mass market. And Tesla buyers simply didn’t care about gap tolerances. The Model Y remains the best-selling BEV globally for a good reason.

But Tesla was only the opening act. What is now emerging from China is something far more systemic: a second wave of challengers, backed not by financially struggling startups but by technology giants like Huawei, that are targeting the very heart of the luxury market. The numbers tell the story.

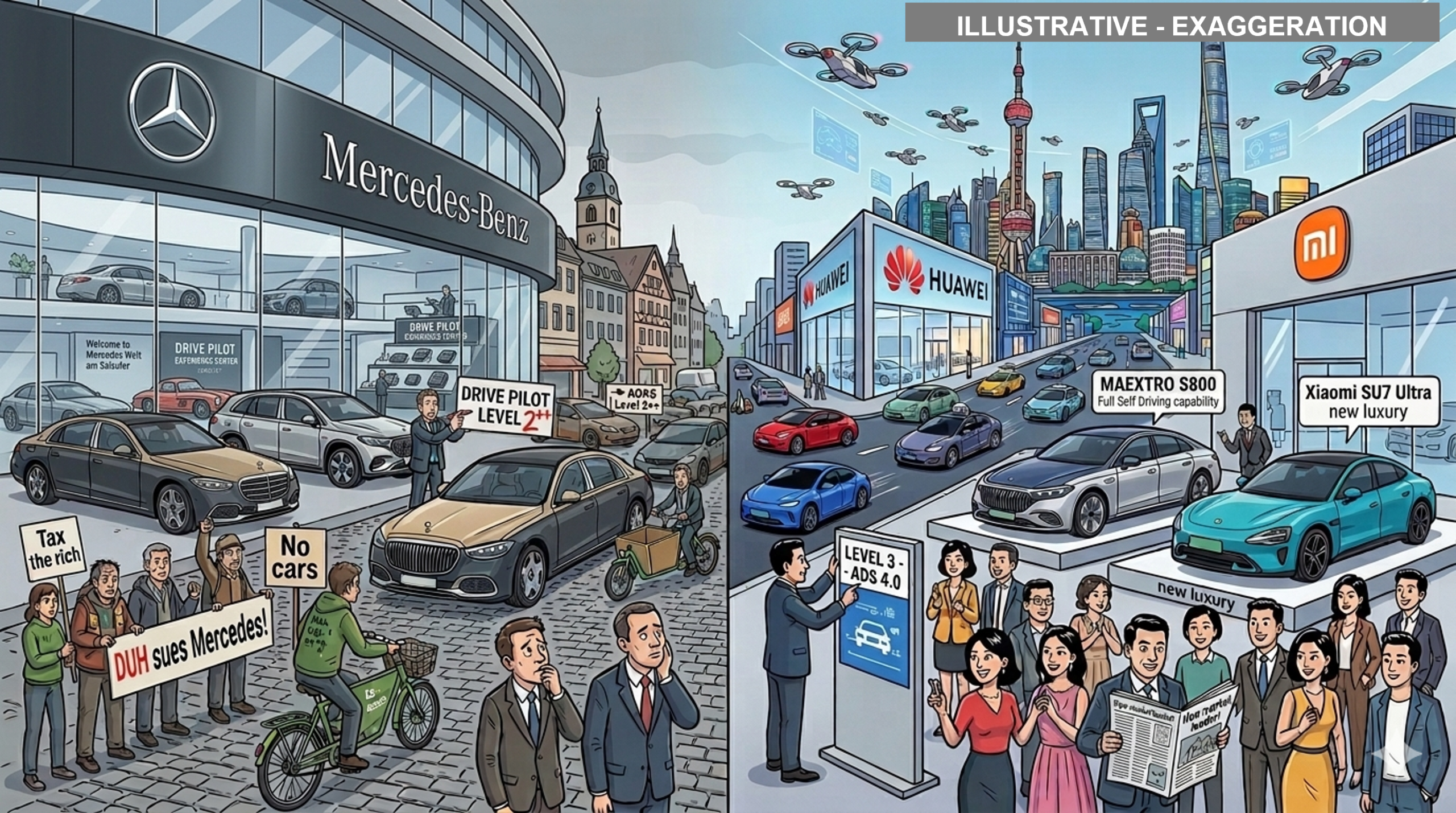

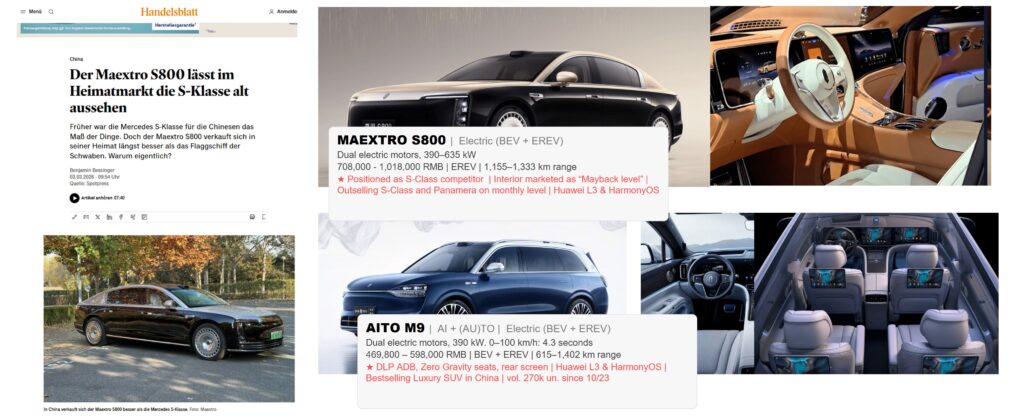

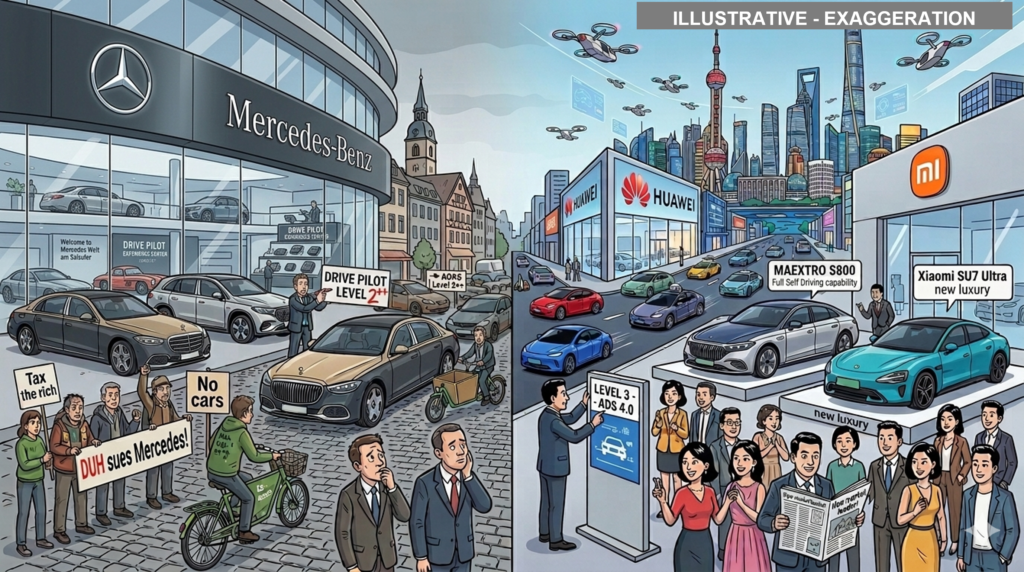

In December 2025, the Huawei-backed Maextro S800 — a luxury sedan priced between 708,000 and over 1,000,000 RMB — set a monthly record of over 4,300 units sold. It outsold the Porsche Panamera, BMW 7 Series, and Mercedes S-Class combined. By January 2026, its cumulative sales had surpassed 14,000 units in barely six months on the market. Maextro plans to launch up to six models in 2026, spanning sedans, SUVs, and MPVs across the 400,000 to 1.3 million yuan range.

Meanwhile, Mercedes-Benz delivered 551,900 vehicles in China in 2025 — a 19% year-on-year decline. BMW sold 625,500 units, down 12.5%. Both companies have declined by more than 10% in China for two consecutive years and cannot get a foothold in China’s booming NEV market, that grew from 4% of passenger vehicle sales in 2019 to >50% in 2025. Forecasts for 2026 suggest production volumes for both brands may soon fall below 500,000 units — levels not seen in a decade.

Understanding Brand Codes: Why Products Are More Than Functions

To understand why this shift is so threatening, one must understand how premium brands actually work in consumers‘ minds. Products in modern consumer society function far beyond their utilitarian value. They are carriers of meaning — symbols that communicate social status, identity, and values. As the semiotician Helene Karmasin argued, consumers buy the statements that products convey, not merely the products themselves.

Successful premium brands encode specific cultural codes — visual, linguistic, symbolic — that consumers decode based on their own cultural context and aspirations. Through consistent design, service experience, and advertising, a brand builds an „aura“ around what would otherwise be a commodity. A Mercedes-Benz S-Class is not just a car that transports you from A to B. It is a statement of dominance, achievement, and belonging to a certain tier of society. This is precisely the mechanism that Chinese challengers are now disrupting.

The Tech-Luxury Revolution: A New Category of Premium

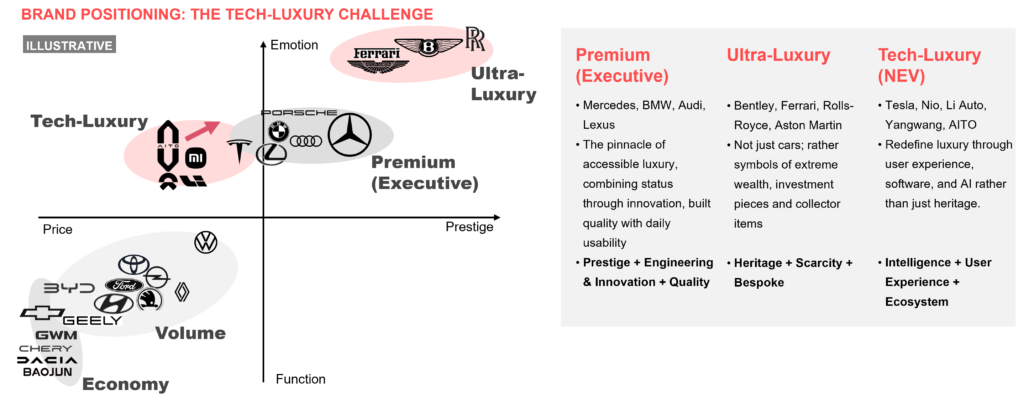

What makes the current challenge fundamentally different from any previous competitive threat is this: Tesla and Chinese tech-luxury brands are not trying to beat German premium brands at their own game. They are creating an entirely new game. The automotive premium market has historically been organized along two dimensions: prestige and emotion. Instead of building emotion through (combustion) engine power and luxury insignia, they play the technology game.

Tech-Luxury brands like Tesla, NIO, Li Auto, Yangwang, AITO, Maextro have redefined luxury through user experience, software, and AI rather than heritage alone. Their statement is Intelligence + User Experience + Ecosystem: Offering a Software-defined Vehicle (SDV) with superior intelligence in infotainment and autonomous driving, offering consumer electronics-like user experience (UX) like a rolling smartphone and access to the brands ecosystem of services and data, may it be Tesla’s supercharger network, driving data that enables FSD (the full self-driving mode) or full integration to Huawei’s HarmonyOS or Xiaomi’s MiUI environment of apps, smart devices and services.

The second wave of NEV players — spearheaded by Huawei’s HIMA alliance and Xiaomi — is pushing aggressively from the tech-luxury quadrant towards premium and ultra-luxury territory. They are not nibbling at the edges. They are redefining what luxury means for an entire generation.

Why Traditional Brand Codes Are Losing Their Power

The traditional codes of German premium — the turbo engine as a symbol of absolute power, the hand-stitched leather as a marker of craftsmanship, the triple-digit top speed as proof of engineering superiority — carry immense weight with existing customer groups in Europe, NAR, and MENA. But in China, which has become the center of gravity of the global premium market, these codes are rapidly losing relevance.

Consider the demographics: China’s luxury car buyers are on average 10–20 years younger than their European or North American counterparts. Many belong to the „second-generation rich“ — the children of China’s first wave of entrepreneurs. They grew up with smartphones, not combustion engines. For them, a 76-inch head-up display, Level 3 autonomous driving, and seamless HarmonyOS integration are not gimmicks. They are the new benchmarks of premium. A V12 or bi-turbo engine does not make them feel like pioneers. It makes them feel like they are driving their father’s car.

The Maextro S800 illustrates this perfectly. It offers 896-channel LiDAR, Huawei’s ADS 4.0 autonomous driving system, a 43-speaker sound system, a starlight ceiling à la Rolls-Royce, and gesture-controlled privacy glass — in a design that purposely challenges Mercedes’s S-Class or even Maybach lineup (by mocking its bi-color paintwork). While Huawei’s ADS 4.0 autonomous driving technology is the ultimate tech statement, Mercedes has just downgraded its autonomous driving ambitions to Level 2++. Chinese consumers are tech-savy and notice these things.

The Only Path Forward: High-Tech Luxury PLUS

So what can German premium brands do? Retreat to their heritage castle and hope the moat holds? That would be a slow death sentence in the world’s largest automotive market.

The only viable strategy is what I call High-Tech Luxury PLUS: maintain the established brand promise of craftsmanship, heritage, and quality while simultaneously matching or exceeding the tech-luxury challengers on their own terms. This is not an either/or. It must be both!

Concretely, this means action on six fronts:

1. Overcome the legacy rucksack — become agile like Tesla or Xiaomi. While traditional German OEMs need four to five years for a development cycle, BYD launches new models in under two years. Xiaomi went from first concept to series production in under three years. This speed gap is not merely inconvenient — it is existential. Establishing startup-like structures within product development, empowering young talent, and ruthlessly simplifying book-like model brochures and variant complexity are prerequisites, not nice-to-haves. Our Operation Phoenix transformation framework, detailed in the forthcoming book „Totalschaden?“, provides a concrete blueprint for this organizational metamorphosis.

2. Pursue a radical consumer-first strategy. German OEMs have a deep tradition of engineering for engineering’s sake — what insiders call „technophilia.“ The result: overengineered features that impress fellow engineers but leave consumers indifferent, while the features Chinese consumers actually crave — seamless smartphone integration, intuitive voice control, 2nd row seat comfort and 7 seats (in SUV / MPV concepts) — lag behind Chinese competitors by years. The antidote is not more NCBS/IQS and clinics, but genuine co-creation: embedding lead users and consumer communities directly into the design and development process, exposing designers and engineers to the real needs and challenges of lead users and developing solutions together, not disconnected in the ivory tower. I pioneered this approach at Volkswagen when we co-created the initial concept of what became the Talagon — VW’s first consumer-co-created model in China. In luxury segments, where standard quantitative research yields shallow insights, qualitative and co-creation approaches are not optional. They are the only methodology that really works.

3. Build technology partnerships with leading players. The era of doing everything in-house is over — if it ever existed. Huawei has demonstrated with its HIMA alliance how a technology player can leverage formerly mediocre OEMs (JAC, Seres, BAIC) into premium and luxury contenders. Mercedes’s MB.OS needs to deliver, and fast — but if it can’t match the pace, strategic partnerships with technology leaders (including, potentially, Chinese ones) may be the pragmatic path. Having facilitated successful technology partnerships in the Chinese market, I can attest: these alliances are complex but achievable when structured as genuine win-win relationships and executed at Chinese speed.

4. Refocus portfolios on value-creating segments. German manufacturers suffer from historically grown portfolios filled with niche models that primarily justify underutilized plants and oversized engineering organizations. In times of declining cash flows, OEMs need the discipline to concentrate on key segments, cash cows, brand icons, and genuine image drivers. Every model that doesn’t earn its place in the portfolio is a drain on resources that could fund the transformation.

5. Define target groups and product statements with precision. Positioning is the key – or as Ries / Trout called it: the success factor in the „battle for the consumer’s mind.“ Their statement „Positioning is not what you do to a product. But what you do to the mind of the prospect.“ boils down to a simple truth: It is not about technological KPIs, benchmark competitors or gap tolerances, it is about an image, a statement and a product story in the consumer’s mind that triggers the purchase and makes the product right for him or her. During my time leading Volkswagen’s product strategy team in China, I positioned the SUV-twins Tharu/T-Roc L and Tiguan/Tayron to target entirely differentiated consumer groups from a virtually identical technological base — with clearly differentiated product stories and use cases, while avoiding substitution and cannibalization. This kind of surgical positioning, grounded in deep socio-demographic understanding, is what separates profitable portfolios from sprawling ones.

6. Root product design in semiotic strategy. The art of premium product positioning and management is not only about technology. It is about storytelling — creating the right statements and codes that resonate with target consumers‘ unconscious desires and social aspirations. This requires translating consumer insights into a coherent product and design concept where the „message“ remains consistent across all touchpoints. I have successfully applied semiotic product design principles to technically define 9+ vehicle models in the Chinese market. The approach works. But it requires product managers who understand both the engineering and the cultural dimension of what they are building.

The Race Is Still Open — But the Clock Is Ticking

Will German premium brands become obsolete? Not yet. The race is still open. Mercedes-Benz retained its leading market share in China’s million-RMB-plus segment in 2025. Chinese ICE sales are growing again in 2026 and market shares of German OEMs are stabilizing. Brand heritage, global recognition, craftsmanship, and residual-value proposition remain formidable assets.

But assets depreciate when left unattended. China-for-China approaches are a crucial first step — but they will not be sufficient in the long run. The redefinition of luxury that started in Beijing and Shanghai will not stay there. It will ripple through Southeast Asia, the Middle East, and eventually reach the doorstep of European and American consumers.

The question is not whether German premium brands can adapt. The question is whether they will — fast enough.

Steffen Edlinger is the founder of Edlinger Strategy & Consulting and author of the forthcoming book „Totalschaden? — Wie Deutschlands Autoindustrie abstürzen konnte und der Fahrplan für den Neustart“ (Q4/2026). With nearly two decades of experience spanning Volkswagen China, HELLA/FORVIA, and PwC Strategy&, he advises automotive OEMs and suppliers on product strategy, transformation, and China market entry.